Jump to winners | Jump to methodology

Young and determined

For this year’s cohort of Insurance Business America’s Rising Stars, the future is so bright they need sunglasses.

“Most companies are hungry for bright, young talent to be their future,” says Rising Star Carrie Cheeks, the southeast territory manager for the workers’ compensation (WC) division of Jencap Insurance Services. “The under 35s are in a great spot for growth and will soon be leaders within our industry.”

“I am skilled in many areas, but I don’t think my personal talents would mean much without the ability and willingness to collaborate with others”

Tamra Johnson, American Property Casualty Insurance Association

Generation Z (born after 1996) have been starting their first jobs while Millennials (born 1980–96) have been bolstering their résumés and are positioned to move into senior-level positions, according to David E. Coons, senior vice president of The Jacobson Group, a global provider of talent to the insurance industry. As Baby Boomers (born 1946–64) and Traditionalists (born 1928–45) retire, Generation X will fill their roles, thereby freeing up opportunities for those 35 and under.

“Generation Z and Millennials are more likely to view work as something you do, not a place you go. They value flexibility, but they also crave connections and collaboration. Given where they are in their careers, many are focused on their next steps professionally,” Coon adds.

Tech-savvy talent

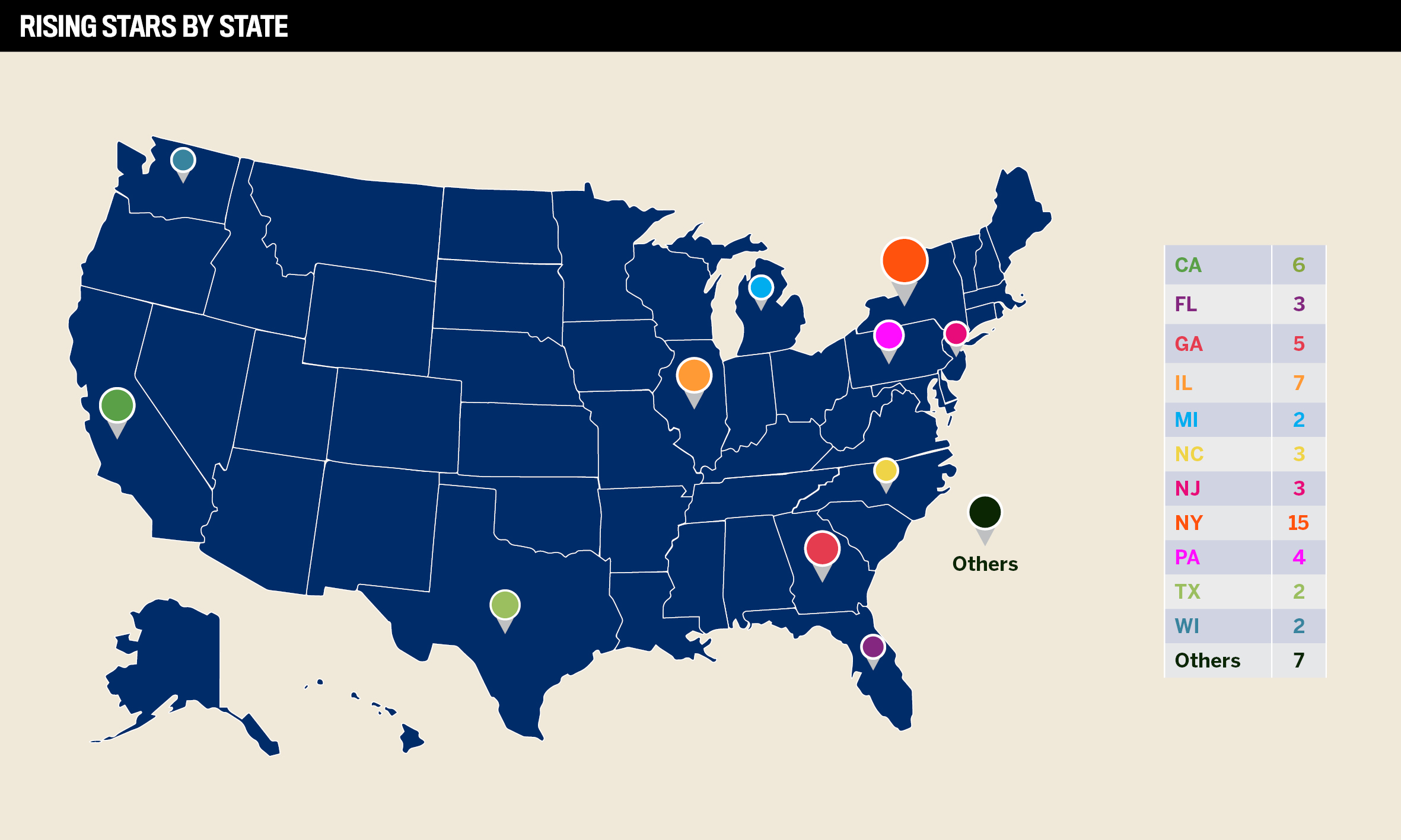

Once again, IBA has selected some of the finest insurance professionals aged 35 and under. The nominees’ roles, achievements, and goals were assessed as well as their contributions to the industry. This year, 59 luminaries were found to be blazing a pathway to excellence.

One of the judging panel, Danette Beck, partner and head of industry verticals and national construction practice leader at USI Insurance Services, says, “The quality and the caliber of talented young professionals who were nominated for the IBA Rising Stars recognition was impressive. I am personally excited for the future of our industry if these are the young men and women leading the charge. The insurance industry will be in great hands.”

Evidently, it’s an opportune time to be in the top tier. Due to an expected increase in volume and some understaffing, most companies are planning to hire new workers over the next 12 months, according to a recent study by the Jacobson Group and Ward. Employment is expected to jump 0.94%.

Still, technology remains a disruptor. Of the small number of companies that plan to cut headcounts, 12% say the reason is improved automation.

National Association of Professional Insurance Agents CEO Mike Becker agrees with this viewpoint. “Attracting top, emerging talent to insurance is so important. For insurance agencies in particular, it’s a critical factor because advancing digital strategies and working with next-generation customers are key to growth. Agents need comprehensive digital strategies, and this is an area where Millennials and Gen Zs can have a big impact. There is good momentum with insurance agencies today, and Millennial and Gen Z agents will be key to sustaining it,” he says.

“There can be a substantial learning curve when someone enters the industry, and it takes time to get fully up to speed”

Allen Canaday, CRC Group

Perseverance pays off

The Rising Stars of 2022 have excelled, but what are the challenges they’ve had to overcome to achieve that?

Cheeks says it’s a matter of perspective, awareness and reputation. “If you don’t know someone in the industry, insurance can be perceived as a poorly lit office full of cubicles and file cabinets,” she explains. “Insurance is so much more. The opportunities are bountiful, but many young professionals lack awareness. Excluding individuals involved in risk management and insurance (RMI) programs, Gamma Iota Sigma, or Invest, the knowledge most young people have of insurance lies within home, auto and healthcare — lines they have experience purchasing. Insurance is typically categorized with a negative experience in someone’s life, creating a subpar reputation for our industry.

“We have the opportunity to retell our story and create a new reputation for insurance.”

Rising Star Allen Canaday, managing director of the CRC Group, concurs for the most part, noting that while the stigma persists that insurance is boring, he’s found it to be flawed. And the trouble with programs such as RMI is that many students don’t know they exist.

During the pandemic, Coons observed that nearly 40% of Generation Z struggled with mental health – compared with 27% of Millennials, 24% of Generation X, 15% of Baby Boomers and 8% of Traditionalists. A study by the Society for Human Resource Management also revealed that “Gen Zers are significantly more likely to feel tired or lacking in energy due to the pandemic, compared to members of other generations. Additionally, more than half of Generation Z reported feeling burned out at work, compared with 24% of Baby Boomers.”

Work-life balance is an issue for another Rising Star, Tamra Johnson. In a previous position, the assistant vice president at American Property Casualty Insurance Association found herself missing commitments with family and friends. “I’ve learned that no matter the career, balance is a challenge for us all. I’ve been inspired by [my] conversations with our leaders at APCIA, members and industry colleagues about how organizations or companies are applying research and development programs to support everyone in the workplace, including parents and caregivers,” she says. “Having these conversations has never been more important, especially as many found themselves working through a pandemic.”

However, Canaday pinpoints a lack of patience from colleagues as a major hurdle to overcome. “There can be a substantial learning curve when someone enters the industry, and it takes time to get fully up to speed,” he says. “It also takes time to build a book of business and strong, trusting relationships with carriers, agents and brokers. Society has become used to stories of instant gratification and overnight success, but in reality, a solid career takes patience, learning from your mistakes, and years of consistent effort to build.”

Meanwhile, Cheeks says comfort, complacency and impatience are primary factors.

“While many young insurance professionals are working hard and climbing the ladder quickly, some continue to remain in the same position,” she explains. “What are the separating factors for these individuals? Those who are climbing continually push their boundaries going above and beyond and doing more than asked. They are working harder to exceed expectations and don’t allow themselves to become comfortable or complacent. They understand the industry is not fair and some colleagues will get a jumpstart. They are happy for others’ success but still have a competitive edge. They understand success doesn’t happen overnight, it’s a process that takes a lot of time and energy. While I’m unsure of exactly what it is that holds young professionals back, this is what has jolted me forward.”

Chelsea Sirovatka, of Risk Placement Services, is another Rising Star. The transportation underwriter cites her age as a cause for people to underestimate her ability. She says, “I would say a major challenge I’ve faced in my career is being younger in this industry. Sometimes people worry that you won’t be as aggressive to get a deal done or you’re not as knowledgeable as someone older.” But Sirovatka stresses she is “still eager to grow” and adds, “considering I have about 35 years left to go in my career, I might as well have fun along the way and to have a personality in this industry is huge.”

“Most companies are hungry for bright, young talent to be their future. The under 35s are in a great spot for growth and will soon be leaders within our industry”

Carrie Cheeks, Jencap Insurance Services

Passing the baton

Managing the generational knowledge gap has been a significant concern, according to Coons. With a lot of people working remotely, it’s been more difficult to facilitate knowledge transfer.

“Most seasoned workers enjoy sharing their expertise and experience with younger colleagues,” he says. “Yet, it can be difficult to recognize when a younger individual is struggling with a particular component of their work in the remote environment.”

To counter this issue, he recommends cultivating a supportive culture with mentorships and meetings.

Johnson can empathize with this, adding, “I am skilled in many areas, but I don’t think my personal talents would mean much without the ability and willingness to collaborate with others.”

“The insurance industry employment market has been very favorable for younger people over the past two years,” says Canaday. “As the older generation starts to look toward retirement, there will continue to be ample opportunity for young talent to step up and prove themselves in a transitioning marketplace. I think this trend will continue as companies work to implement and expand their leadership programs.”

This learning curve is being helped by mentorship schemes in the industry. “In the past, there’s been a big focus on experience, experience, experience and you’re seeing some insurers now being more open to some of the softer skills as a priority, explains Marguerite Murer Tortorello, managing director of Insurance Careers Movement. “And then if you go to those seasoned professionals, they are helping them provide mentoring opportunities to bridge that gap of years of experience.”

After starting out as an underwriting assistant in 2016, Canaday rose to his current director role in 2020, where he oversees a P&C binding authority team writing business in all 50 states. During his tenure, he’s grown his book of business to more than $2 million in revenue.

Carmen McKeon, office president at CRC, adds, “Allen continues to be a team player, never asking more of his team than he ask of himself. He works hard to provide insight in efficiencies in processes, tracking revenue for each region, making marketing visits with his team and answering day-to-day questions around underwriting, systems and how to provide solutions when problems arise. We started this unit with a zero, and he has been a constant to an ever-changing start-up opportunity to generate revenue for our organization.”

How does Canaday see the industry? With the hardening market, he says, the property space is more selective with its total insurable value limits – making things more difficult with increased construction cost – and there are several industries with fewer markets available on the casualty side.

Cheeks sees a similar dynamic for the labor market. “There is so much opportunity in the insurance market,” she says. “It is no secret our industry is aging. Over the last few years, companies have certainly started to take a more serious approach to finding solutions to our aging workforce.”

Cheeks is responsible for the growth of Jencap’s WC book and agency and carrier relationships across the southeast region. She started out in 2018 as a small accounts new business broker in Georgia with under $15,000 in premium. Soon, she was not only doing business throughout the east coast but also managing approximately 500 accounts per month and binding around 75.

“Our WC book has seen double-digit increases in the last few years as rates, on average, continue to decrease nationally,” she says.

Jencap’s managing director of sales Paul Orlando compliments Cheeks’ achievement, saying, “She’s hands down one of our best territory managers in the company. Carrie is always on the clock helping her agents at the 11th hour if necessary. I don’t think I’ve ever not gotten a call back from her within an hour or so. That’s hard to find these days. Every time we speak, Carrie is offering up new ideas and solutions to help better our sales team at large.”

Regarding market trends, Cheeks describes the workers’ compensation segment as soft. “Rates are at an all-time low with no bottom in sight. WC is in its eighth year of profitability. The rise of inflation has yet to play a role in the increase of WC rates, and it may never be the driving force behind a turn in the marketplace,” she says.

“Increases in salaries and minimum wage have bolstered the payrolls, causing an increase in WC premiums. Additionally, there has been more of a focus on workplace safety in the last decade that will only increase in years to come. The rise of technology in insurance will continue to assist in this movement.”

- Alessandra Rohde

Head of Customer Success

Broker Buddha

- Alex Luxenburg

Senior Vice President

CAC Specialty

- Alexis Nicole Gutierrez

Agency Owner/Principal

New Era Insurance

- Alexis Spoon

Area Assistant Vice President

Gallagher

- Alicia Golia

Director of Cyber and Technology Insurance Solutions

Ambridge Partners

- Andrew Notohamiprodjo

Data Scientist

Delos Insurance Solutions

- Andrew Silva

Senior Financial Lines Manager

Woodruff Sawyer

- Angela Oroian

President

Society of Environmental Insurance Professionals

- Angela Rimgaila

Assistant Vice President, Underwriting, Management Liability

IAT Insurance Group

- Ben Coe

Partner

Shepherd Insurance

- Brandon Behun

Director of Analytics, Underwriting, and Innovation

HUB International

- Brett Davis

Senior Business Development Specialist

GS Insurance Solutions

- Britany LaManna

Senior Account Executive

The Loomis Company

- Christopher Clementi

Assistant Vice President

CNA Insurance

- Dan Sweet

Assistant Vice President, Healthcare Practice

USI Insurance Services

- Dean Hoski

Assistant Vice President, Underwriting

Crum & Forster

- Drew Barker

Sales Account Manager I

American Modern Insurance Group

- Erich Lowe

Senior Vice President, Team Leader

Aon

- Francesca Barbano

Employee Benefits Consultant

HUB International

- Gerald Fawcett

Senior Vice President, Property and Casualty Practice Leader

The Plexus Groupe

- Heather Billingslea

Assistant Vice President, Personal Risk Manager

Chubb

- Jaime Mann

Vice President, Regional Underwriting Manager

Chubb

- Jared Bower

Vice President and Commercial Lines Manager

HUB International Northeast

- Jason Minnella

Senior Vice President

HUB International Northeast

- John Dewart

Senior Broker, Casualty

Burns & Wilcox

- John Horneff

Founder and Chief Executive Officer

Noldor

- Jon D. Hongsermeier

Agent

Adams Insurance Advisors

- Kayla Livingston

Associate

Nicolaides Fink Thorpe Michaelides Sullivan LLP

- Kelley Holmes

Account Executive, Broadspire

Crawford & Company

- Kenny Eisman

Assistant Vice President

HUB International Northeast

- Khris Dai

Vice President, Actuary

Aon

- Kilauren McShea

Director, US Management Liability

Intact Insurance Specialty Solutions

- Kristen Darling

Vice President, Team Lead

Lockton Companies

- Kristen Nevins

Director of Marketing & Operations

Direct Connection Advertising & Marketing

- Lance Fraser

Senior Vice President, Transactional Risk

Chubb

- Lindsey Jordan

Assistant Vice President, Operations Manager

Personal Risk Management Solutions

- Megan Pittelli

Senior Account Executive

Aon

- Sarah Chandonnet

Underwriting Manager, Private Client Division

Burns & Wilcox

- Sarah Lopez

Claims Specialist

Gallagher Bassett

- Spencer Friedman

Risk Management Consultant

Alera Group

- Sydney Hedberg

Director, MMC Advantage

Marsh McLennan

- Tandeka Nomvete

Director, External Engagement

Spencer Educational Foundation

- Utsav Ratra

Executive Underwriter

Canopius Group

Starting in June, Insurance Business America invited insurance professionals across the country to nominate the most exceptional young talent for the annual Rising Stars list.

Nominees had to be age 35 or under (as of September 30, 2022) and be committed to a career in insurance with a clear passion for the industry. To maintain a focus on new talent, only nominees who hadn’t been previously recognized as Rising Stars (or Young Guns) were considered.

Nominees were asked about their current role, key achievements, career goals and the contributions they’ve made to shaping the industry. Recommendations from managers and senior industry professionals were also taken into account.

The final list of 59 Rising Stars was determined by an independent panel of industry leaders:

• Jennifer Wilson, director of specialty claims and contracts at Hub International

• Danette Beck, national construction practice leader at USI Insurance Services

• Angela Dybdahl Oroian, MS, president and managing director at Society of Environmental Insurance Professionals (SEIP)

• Margaret Redd, executive director at the National African-American Insurance Association (NAAIA)

• Sandy Locke, chief people officer for reinsurance solutions and human capital solutions at Aon

The 2022 Rising Stars special report is proudly supported by the Latin American Association of Insurance Agencies and Big I.

Source link

2022-10-25 12:00:00

https://ift.tt/cZ5q1Fw